Spend crypto seamlessly with your Debit card

Spend crypto seamlessly with your Debit card

Spend crypto seamlessly with your Debit card

Spend crypto seamlessly with your Debit card

2022-2023

2022-2023

2022-2023

2022-2023

Overview

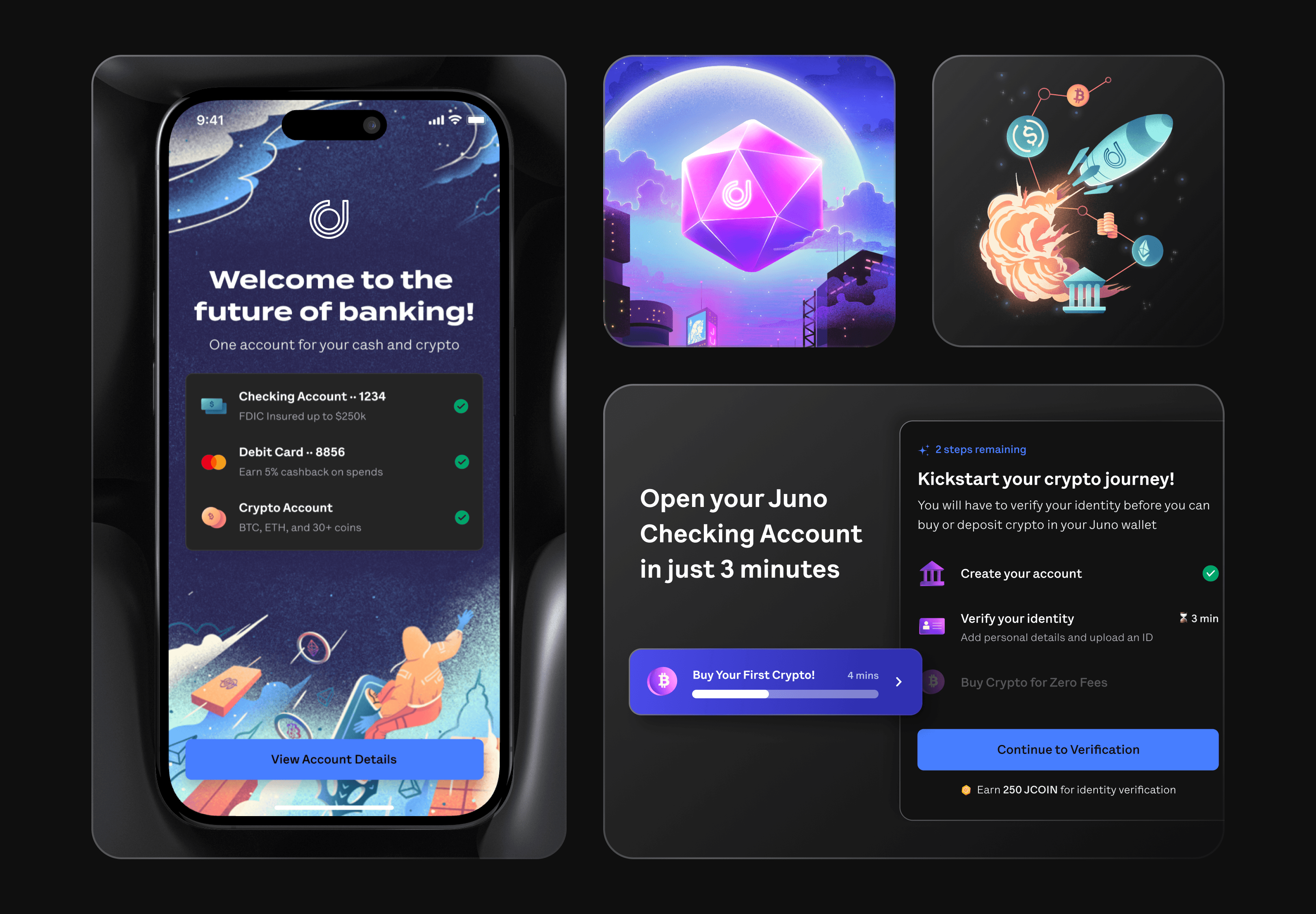

Enabling users to open a Global account with Juno to deposit crypto and spend it anywhere in the world through their virtual debit card within a few minutes of opening their account. Also allowing users to refer their friends and choose & order a debit card.

Role

:

Sr. Product Designer

Client

:

Juno Finance

Website

:

https://juno.finance/

Timeline

:

4 months

Problem Statement

Many banks didn't let people move money from crypto exchanges, causing difficulties for those wanting to turn their crypto into fiat money. People who earned in crypto wanted more accessible ways to spend it for daily things. Also, some debit cards charged a lot for international use, and some big companies in the US didn't take payments from certain international cards, affecting approximately 23% of their potential user base.

Many banks didn't let people move money from crypto exchanges, causing difficulties for those wanting to turn their crypto into fiat money. People who earned in crypto wanted more accessible ways to spend it for daily things. Also, some debit cards charged a lot for international use, and some big companies in the US didn't take payments from certain international cards, affecting approximately 23% of their potential user base.

Many banks didn't let people move money from crypto exchanges, causing difficulties for those wanting to turn their crypto into fiat money. People who earned in crypto wanted more accessible ways to spend it for daily things. Also, some debit cards charged a lot for international use, and some big companies in the US didn't take payments from certain international cards, affecting approximately 23% of their potential user base.

Many banks didn't let people move money from crypto exchanges, causing difficulties for those wanting to turn their crypto into fiat money. People who earned in crypto wanted more accessible ways to spend it for daily things. Also, some debit cards charged a lot for international use, and some big companies in the US didn't take payments from certain international cards, affecting approximately 23% of their potential user base.

User and Market Research

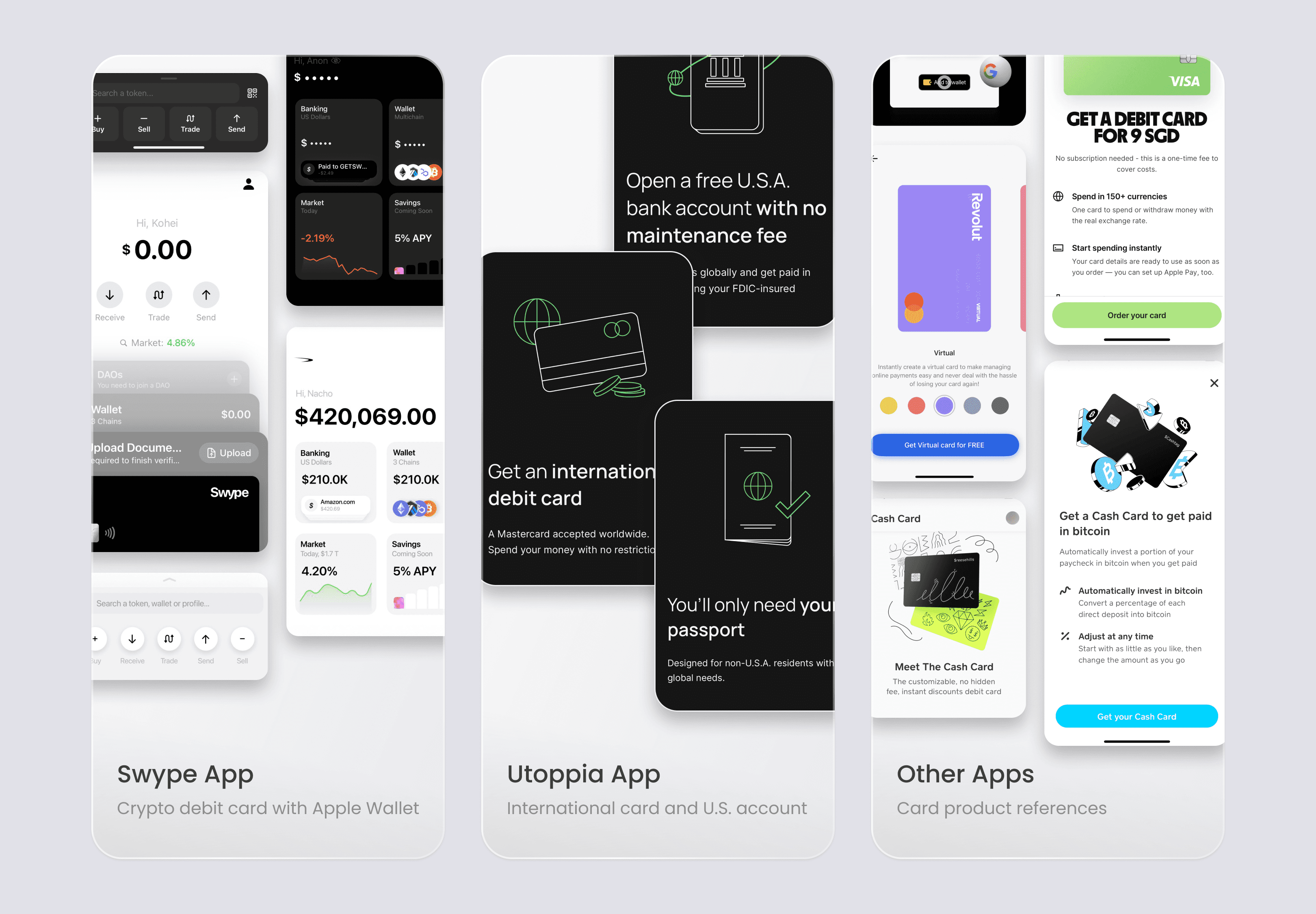

We extensively researched global finTech and crypto apps, mainly focusing on those supporting US bank accounts worldwide and/or offering a crypto card product.

Our investigations revealed that existing crypto card spending products like Swype were slow due to inadequate fiat or checking account infrastructure. This resulted in a long time for fund movement and settlement, leading to inconvenience during transactions.

Among the challenges faced by global travelers using cards were exorbitant forex charges and hidden fees, adding to user dissatisfaction.

A loss of faith in traditional centralized financial systems drove a growing demand for earning and spending in crypto. Compounded by banks restricting transfers from crypto exchanges, individuals receiving payments in crypto encountered obstacles in converting to fiat. Moreover, the off-ramp fees on other platforms were notably high.

Many US-based apps required payments from specific countries or issued cards exclusively through US banks. This posed difficulties for widely used platforms like Notion and Figma, creating payment hurdles.

We already had a fully operational checking account with our partner bank and a crypto exchange within the Juno app. We could achieve seamless fund transfers and rapid settlements. This setup resulted in an exceptional user experience.

We extensively researched global finTech and crypto apps, mainly focusing on those supporting US bank accounts worldwide and/or offering a crypto card product.

Our investigations revealed that existing crypto card spending products like Swype were slow due to inadequate fiat or checking account infrastructure. This resulted in a long time for fund movement and settlement, leading to inconvenience during transactions.

Among the challenges faced by global travelers using cards were exorbitant forex charges and hidden fees, adding to user dissatisfaction.

A loss of faith in traditional centralized financial systems drove a growing demand for earning and spending in crypto. Compounded by banks restricting transfers from crypto exchanges, individuals receiving payments in crypto encountered obstacles in converting to fiat. Moreover, the off-ramp fees on other platforms were notably high.

Many US-based apps required payments from specific countries or issued cards exclusively through US banks. This posed difficulties for widely used platforms like Notion and Figma, creating payment hurdles.

We already had a fully operational checking account with our partner bank and a crypto exchange within the Juno app. We could achieve seamless fund transfers and rapid settlements. This setup resulted in an exceptional user experience.

We extensively researched global finTech and crypto apps, mainly focusing on those supporting US bank accounts worldwide and/or offering a crypto card product.

Our investigations revealed that existing crypto card spending products like Swype were slow due to inadequate fiat or checking account infrastructure. This resulted in a long time for fund movement and settlement, leading to inconvenience during transactions.

Among the challenges faced by global travelers using cards were exorbitant forex charges and hidden fees, adding to user dissatisfaction.

A loss of faith in traditional centralized financial systems drove a growing demand for earning and spending in crypto. Compounded by banks restricting transfers from crypto exchanges, individuals receiving payments in crypto encountered obstacles in converting to fiat. Moreover, the off-ramp fees on other platforms were notably high.

Many US-based apps required payments from specific countries or issued cards exclusively through US banks. This posed difficulties for widely used platforms like Notion and Figma, creating payment hurdles.

We already had a fully operational checking account with our partner bank and a crypto exchange within the Juno app. We could achieve seamless fund transfers and rapid settlements. This setup resulted in an exceptional user experience.

We extensively researched global finTech and crypto apps, mainly focusing on those supporting US bank accounts worldwide and/or offering a crypto card product.

Our investigations revealed that existing crypto card spending products like Swype were slow due to inadequate fiat or checking account infrastructure. This resulted in a long time for fund movement and settlement, leading to inconvenience during transactions.

Among the challenges faced by global travelers using cards were exorbitant forex charges and hidden fees, adding to user dissatisfaction.

A loss of faith in traditional centralized financial systems drove a growing demand for earning and spending in crypto. Compounded by banks restricting transfers from crypto exchanges, individuals receiving payments in crypto encountered obstacles in converting to fiat. Moreover, the off-ramp fees on other platforms were notably high.

Many US-based apps required payments from specific countries or issued cards exclusively through US banks. This posed difficulties for widely used platforms like Notion and Figma, creating payment hurdles.

We already had a fully operational checking account with our partner bank and a crypto exchange within the Juno app. We could achieve seamless fund transfers and rapid settlements. This setup resulted in an exceptional user experience.

Ideation and Journey

We introduced Juno as a global debit card product instead of a crypto-checking account, catering to a diverse audience outside the US. Through extensive user interviews, we identified pain points and conducted a small beta launch in Q4 of 2022 by redesigning multiple flows in the product.

Crafting an innovative and exciting flow, we ventured into uncharted territory, especially since there was no crypto card product in India then.

Tailoring to our global users, we redefined the 'Aha Moment': the thrill of swiftly funding their crypto wallet and making purchases with crypto at their favorite brands or outlets, unlike the 'Aha Moment' for our US app, which focused on the speed of converting between crypto and fiat within the same banking app.

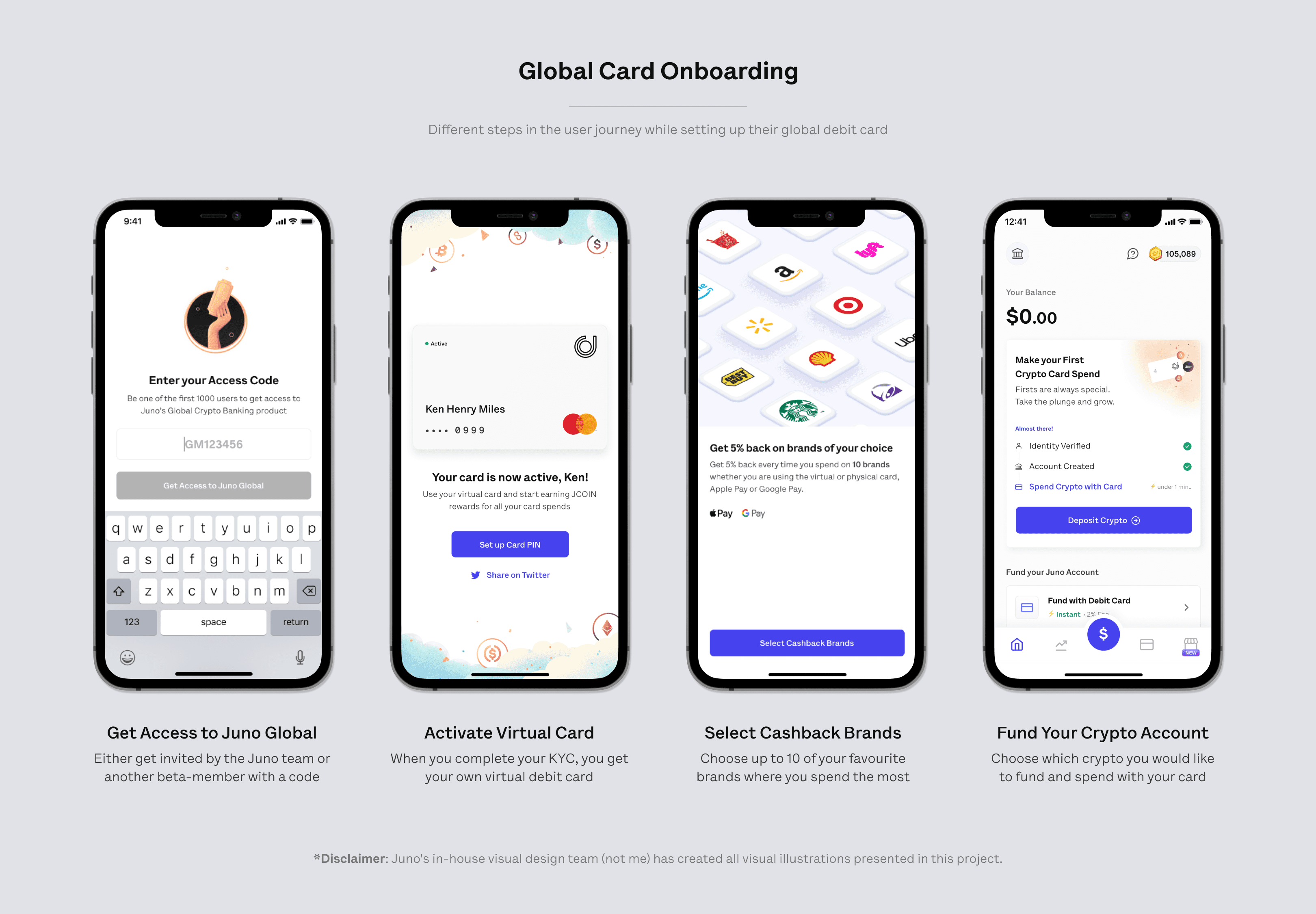

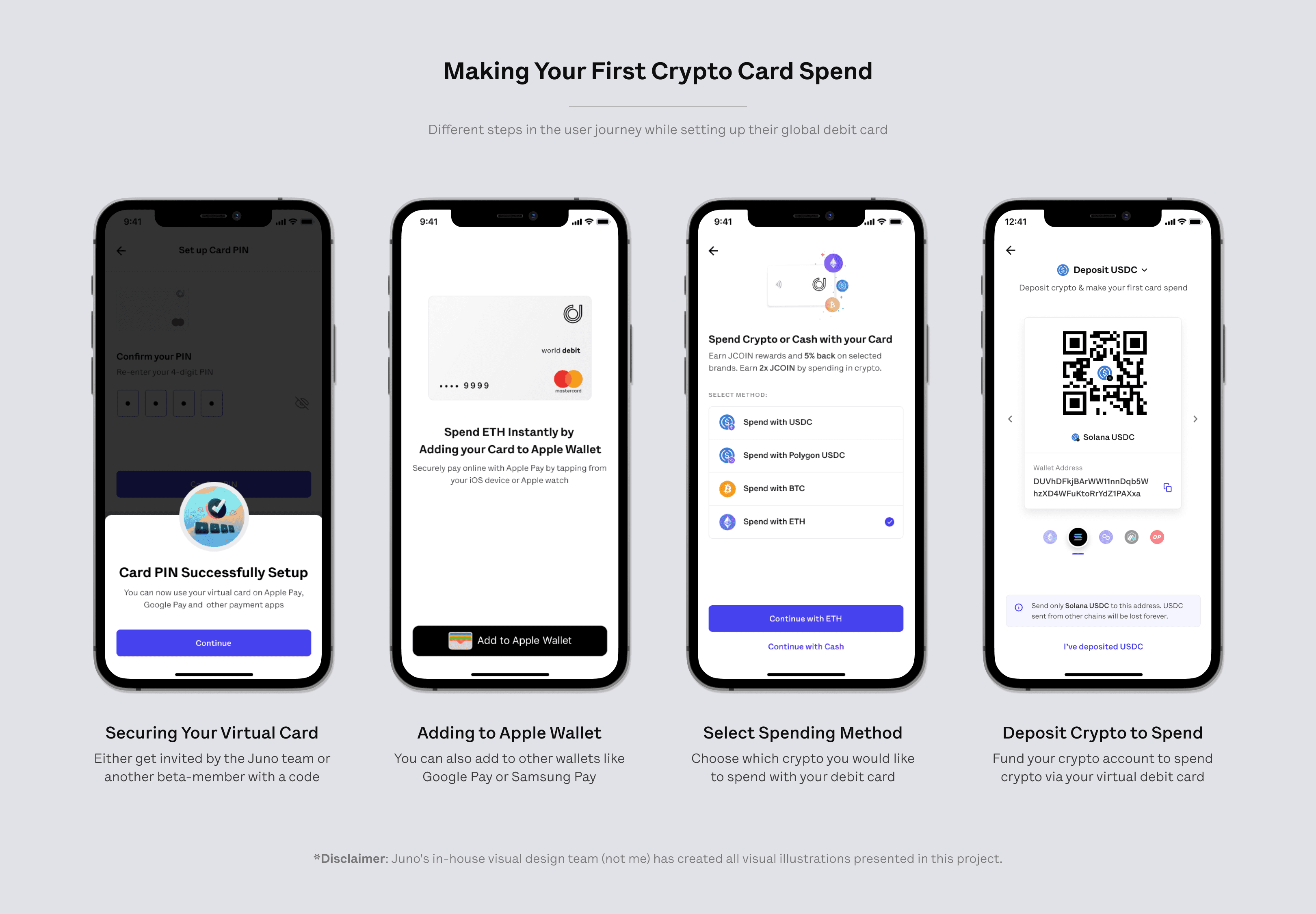

Our onboarding approach differed significantly, requiring only a passport as an ID instead of the typical SSN and ID proof. We prioritized activating their card first, prompting them to fund the wallet for their first crypto card spend.

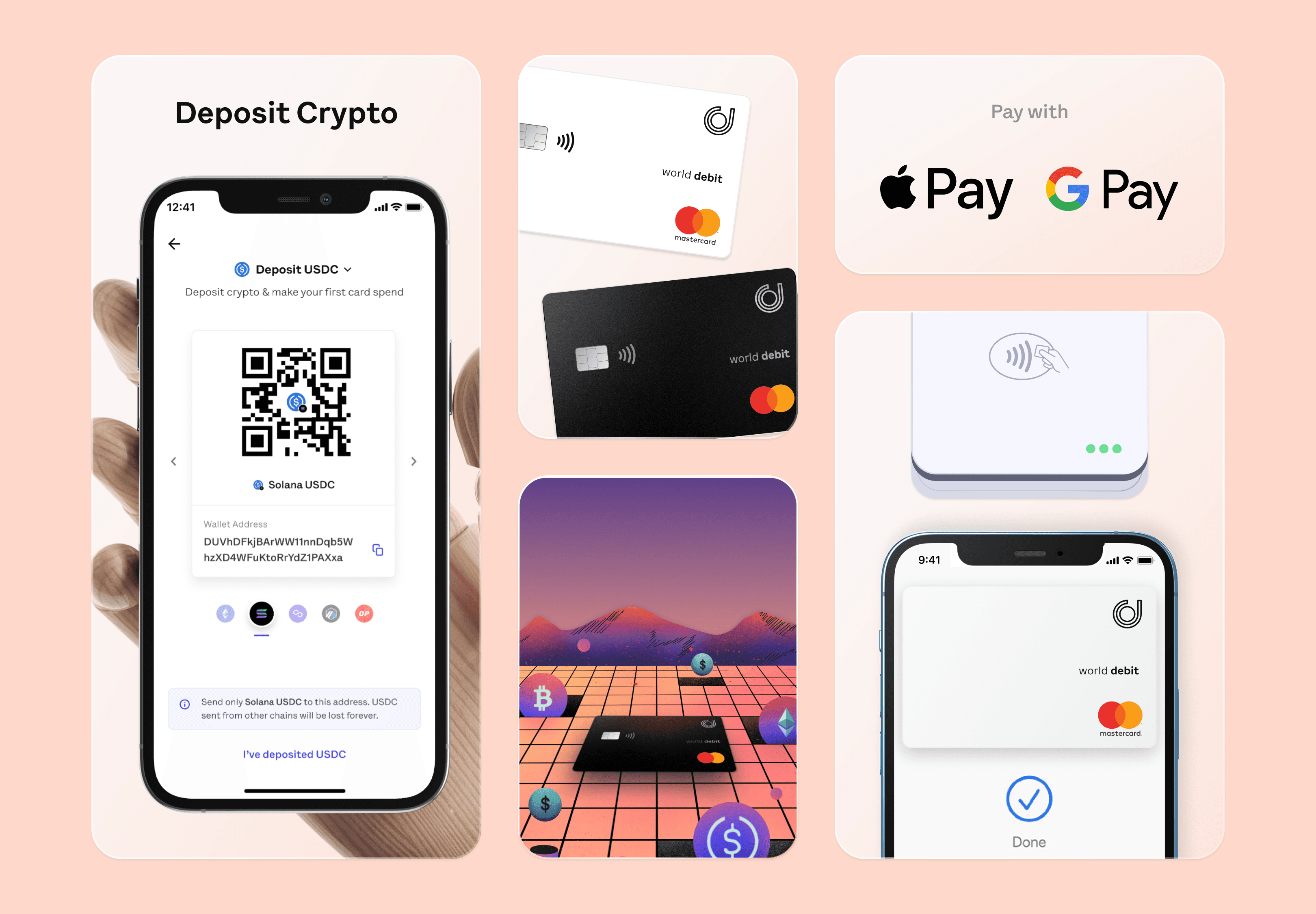

Users were given the choice of 3 cryptos—BTC, ETH, and USDC—across different chains such as Bitcoin, Ethereum Mainnet, Polygon, and Solana. Once funded, they could seamlessly add their virtual card to popular wallet apps like Apple Pay, Google Pay, or Samsung Pay, enabling easy tap-to-pay transactions from Phones or Watches.

We introduced Juno as a global debit card product instead of a crypto-checking account, catering to a diverse audience outside the US. Through extensive user interviews, we identified pain points and conducted a small beta launch in Q4 of 2022 by redesigning multiple flows in the product.

Crafting an innovative and exciting flow, we ventured into uncharted territory, especially since there was no crypto card product in India then.

Tailoring to our global users, we redefined the 'Aha Moment': the thrill of swiftly funding their crypto wallet and making purchases with crypto at their favorite brands or outlets, unlike the 'Aha Moment' for our US app, which focused on the speed of converting between crypto and fiat within the same banking app.

Our onboarding approach differed significantly, requiring only a passport as an ID instead of the typical SSN and ID proof. We prioritized activating their card first, prompting them to fund the wallet for their first crypto card spend.

Users were given the choice of 3 cryptos—BTC, ETH, and USDC—across different chains such as Bitcoin, Ethereum Mainnet, Polygon, and Solana. Once funded, they could seamlessly add their virtual card to popular wallet apps like Apple Pay, Google Pay, or Samsung Pay, enabling easy tap-to-pay transactions from Phones or Watches.

We introduced Juno as a global debit card product instead of a crypto-checking account, catering to a diverse audience outside the US. Through extensive user interviews, we identified pain points and conducted a small beta launch in Q4 of 2022 by redesigning multiple flows in the product.

Crafting an innovative and exciting flow, we ventured into uncharted territory, especially since there was no crypto card product in India then.

Tailoring to our global users, we redefined the 'Aha Moment': the thrill of swiftly funding their crypto wallet and making purchases with crypto at their favorite brands or outlets, unlike the 'Aha Moment' for our US app, which focused on the speed of converting between crypto and fiat within the same banking app.

Our onboarding approach differed significantly, requiring only a passport as an ID instead of the typical SSN and ID proof. We prioritized activating their card first, prompting them to fund the wallet for their first crypto card spend.

Users were given the choice of 3 cryptos—BTC, ETH, and USDC—across different chains such as Bitcoin, Ethereum Mainnet, Polygon, and Solana. Once funded, they could seamlessly add their virtual card to popular wallet apps like Apple Pay, Google Pay, or Samsung Pay, enabling easy tap-to-pay transactions from Phones or Watches.

We introduced Juno as a global debit card product instead of a crypto-checking account, catering to a diverse audience outside the US. Through extensive user interviews, we identified pain points and conducted a small beta launch in Q4 of 2022 by redesigning multiple flows in the product.

Crafting an innovative and exciting flow, we ventured into uncharted territory, especially since there was no crypto card product in India then.

Tailoring to our global users, we redefined the 'Aha Moment': the thrill of swiftly funding their crypto wallet and making purchases with crypto at their favorite brands or outlets, unlike the 'Aha Moment' for our US app, which focused on the speed of converting between crypto and fiat within the same banking app.

Our onboarding approach differed significantly, requiring only a passport as an ID instead of the typical SSN and ID proof. We prioritized activating their card first, prompting them to fund the wallet for their first crypto card spend.

Users were given the choice of 3 cryptos—BTC, ETH, and USDC—across different chains such as Bitcoin, Ethereum Mainnet, Polygon, and Solana. Once funded, they could seamlessly add their virtual card to popular wallet apps like Apple Pay, Google Pay, or Samsung Pay, enabling easy tap-to-pay transactions from Phones or Watches.

This swift process, powered by crypto funding, meant users could create an account and begin spending with their virtual cards within 10-15 minutes.

Our beta launch coincided with ETH India 2022, generating significant buzz during the event. I had the pleasure of meeting some of our beta users in person at the conference, further highlighting the impact of our product.

In the beta launch phase, we aimed to attract only the crypto-native audience, prioritizing exclusivity. Initially, we distributed invites for our access gated app through Twitter to friends within the crypto startup community, yielding valuable and actionable feedback.

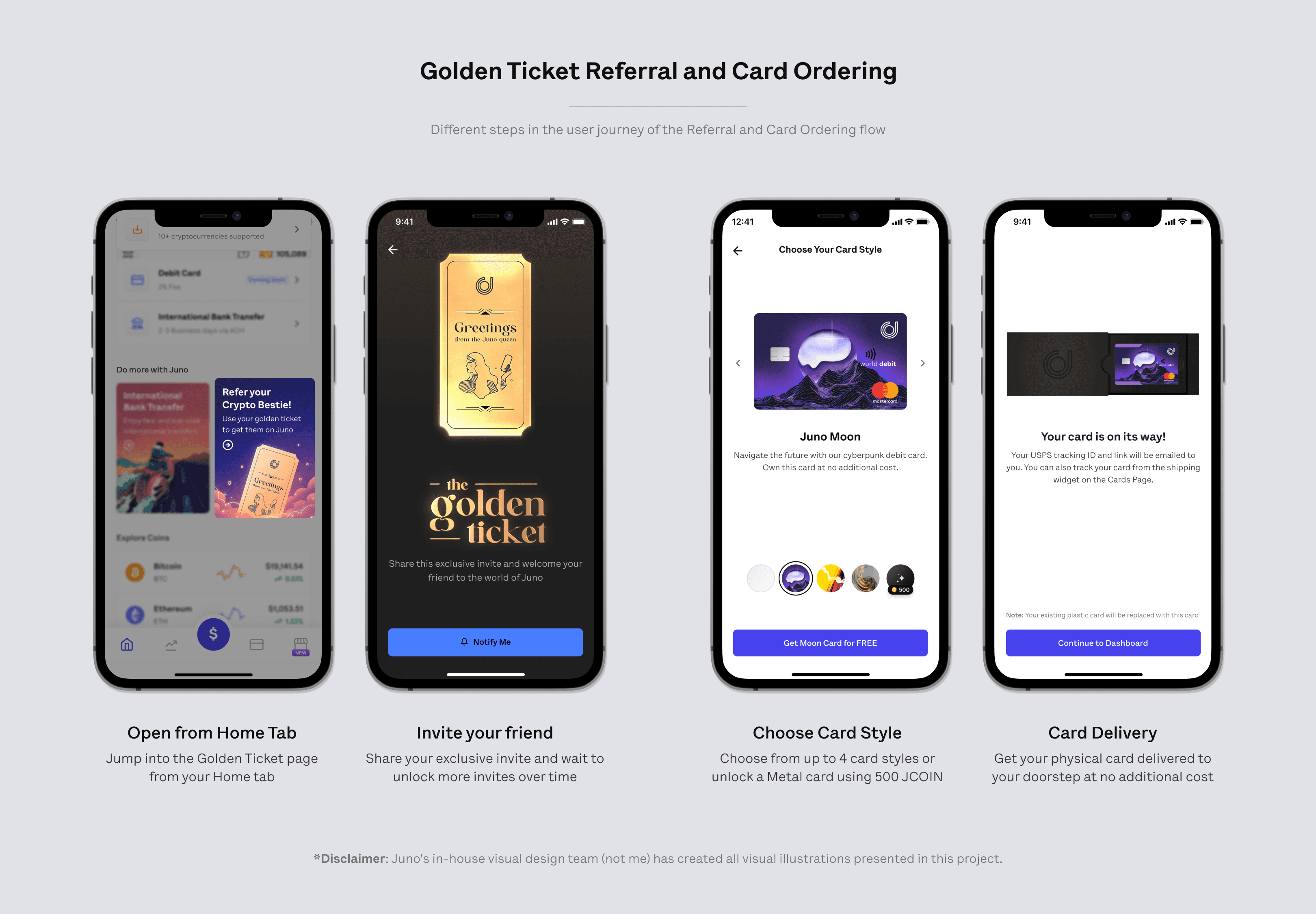

Introducing the 'Golden Ticket' referral program, we restricted users to a single invite, unlocking additional invites as their referred friends joined and made their first crypto card transactions.

Exclusivity effectively attracted high-quality users and generated substantial buzz around our product.

This swift process, powered by crypto funding, meant users could create an account and begin spending with their virtual cards within 10-15 minutes.

Our beta launch coincided with ETH India 2022, generating significant buzz during the event. I had the pleasure of meeting some of our beta users in person at the conference, further highlighting the impact of our product.

In the beta launch phase, we aimed to attract only the crypto-native audience, prioritizing exclusivity. Initially, we distributed invites for our access gated app through Twitter to friends within the crypto startup community, yielding valuable and actionable feedback.

Introducing the 'Golden Ticket' referral program, we restricted users to a single invite, unlocking additional invites as their referred friends joined and made their first crypto card transactions.

Exclusivity effectively attracted high-quality users and generated substantial buzz around our product.

This swift process, powered by crypto funding, meant users could create an account and begin spending with their virtual cards within 10-15 minutes.

Our beta launch coincided with ETH India 2022, generating significant buzz during the event. I had the pleasure of meeting some of our beta users in person at the conference, further highlighting the impact of our product.

In the beta launch phase, we aimed to attract only the crypto-native audience, prioritizing exclusivity. Initially, we distributed invites for our access gated app through Twitter to friends within the crypto startup community, yielding valuable and actionable feedback.

Introducing the 'Golden Ticket' referral program, we restricted users to a single invite, unlocking additional invites as their referred friends joined and made their first crypto card transactions.

Exclusivity effectively attracted high-quality users and generated substantial buzz around our product.

This swift process, powered by crypto funding, meant users could create an account and begin spending with their virtual cards within 10-15 minutes.

Our beta launch coincided with ETH India 2022, generating significant buzz during the event. I had the pleasure of meeting some of our beta users in person at the conference, further highlighting the impact of our product.

In the beta launch phase, we aimed to attract only the crypto-native audience, prioritizing exclusivity. Initially, we distributed invites for our access gated app through Twitter to friends within the crypto startup community, yielding valuable and actionable feedback.

Introducing the 'Golden Ticket' referral program, we restricted users to a single invite, unlocking additional invites as their referred friends joined and made their first crypto card transactions.

Exclusivity effectively attracted high-quality users and generated substantial buzz around our product.

With our physical cards successfully shipping in the US, our card vendors and delivery partners were primed for scale. Extending this approach globally, we crafted plans to identify international vendors to distribute our physical debit cards.

We introduced card personalization options to enhance user engagement, offering users a selection from 5 distinct card styles. Additionally, users could unlock a premium Metallic card using their JCOIN l (in-app loyalty points).

However, our global expansion plans were halted due to compliance constraints, preventing us from advancing to the stage of securing international delivery partners.

With our physical cards successfully shipping in the US, our card vendors and delivery partners were primed for scale. Extending this approach globally, we crafted plans to identify international vendors to distribute our physical debit cards.

We introduced card personalization options to enhance user engagement, offering users a selection from 5 distinct card styles. Additionally, users could unlock a premium Metallic card using their JCOIN l (in-app loyalty points).

However, our global expansion plans were halted due to compliance constraints, preventing us from advancing to the stage of securing international delivery partners.

With our physical cards successfully shipping in the US, our card vendors and delivery partners were primed for scale. Extending this approach globally, we crafted plans to identify international vendors to distribute our physical debit cards.

We introduced card personalization options to enhance user engagement, offering users a selection from 5 distinct card styles. Additionally, users could unlock a premium Metallic card using their JCOIN l (in-app loyalty points).

However, our global expansion plans were halted due to compliance constraints, preventing us from advancing to the stage of securing international delivery partners.

With our physical cards successfully shipping in the US, our card vendors and delivery partners were primed for scale. Extending this approach globally, we crafted plans to identify international vendors to distribute our physical debit cards.

We introduced card personalization options to enhance user engagement, offering users a selection from 5 distinct card styles. Additionally, users could unlock a premium Metallic card using their JCOIN l (in-app loyalty points).

However, our global expansion plans were halted due to compliance constraints, preventing us from advancing to the stage of securing international delivery partners.

Final Prototype

Click here ↗ to interact with the Figma prototype to experience the Global Card Onboarding and Golden Ticket Referral flow

Click here ↗ to interact with the Figma prototype to experience the Global Card Onboarding and Golden Ticket Referral flow

Click here ↗ to interact with the Figma prototype to experience the Global Card Onboarding and Golden Ticket Referral flow

Click here ↗ to interact with the Figma prototype to experience the Global Card Onboarding and Golden Ticket Referral flow

Implementation

In terms of roles:

I was the sole product designer on this project who overlooked the onboarding and referral flows. Two talented in-house visual designers, Trina and Anisha, made the illustrations.

I collaborated directly with the Chief Product Officer, Swam, and the Head of Product, Pratik, to design the flows.

I created web and mobile versions of screens and worked directly with one or two developers from each web, iOS, and Android team.

We followed an iterative approach, revisiting our flows through multiple user testing sessions. We also completed many design reviews to polish how developers implemented design before launching it to our users.

In terms of roles:

I was the sole product designer on this project who overlooked the onboarding and referral flows. Two talented in-house visual designers, Trina and Anisha, made the illustrations.

I collaborated directly with the Chief Product Officer, Swam, and the Head of Product, Pratik, to design the flows.

I created web and mobile versions of screens and worked directly with one or two developers from each web, iOS, and Android team.

We followed an iterative approach, revisiting our flows through multiple user testing sessions. We also completed many design reviews to polish how developers implemented design before launching it to our users.

In terms of roles:

I was the sole product designer on this project who overlooked the onboarding and referral flows. Two talented in-house visual designers, Trina and Anisha, made the illustrations.

I collaborated directly with the Chief Product Officer, Swam, and the Head of Product, Pratik, to design the flows.

I created web and mobile versions of screens and worked directly with one or two developers from each web, iOS, and Android team.

We followed an iterative approach, revisiting our flows through multiple user testing sessions. We also completed many design reviews to polish how developers implemented design before launching it to our users.

In terms of roles:

I was the sole product designer on this project who overlooked the onboarding and referral flows. Two talented in-house visual designers, Trina and Anisha, made the illustrations.

I collaborated directly with the Chief Product Officer, Swam, and the Head of Product, Pratik, to design the flows.

I created web and mobile versions of screens and worked directly with one or two developers from each web, iOS, and Android team.

We followed an iterative approach, revisiting our flows through multiple user testing sessions. We also completed many design reviews to polish how developers implemented design before launching it to our users.

Result and Impact

Our focus had primarily been on the United States market. However, in September 2022, we expanded Juno's product globally and initiated a beta launch involving approximately 150 users from India and Dubai.

Despite having the technology and designs ready for the full launch, we encountered compliance hurdles with our partner bank, restricting further user acquisition and resulting in a halt to the product expansion.

The product remained available to users for 3-5 months. However, a limited beta user cohort only resulted in minimal movement in our business metrics.

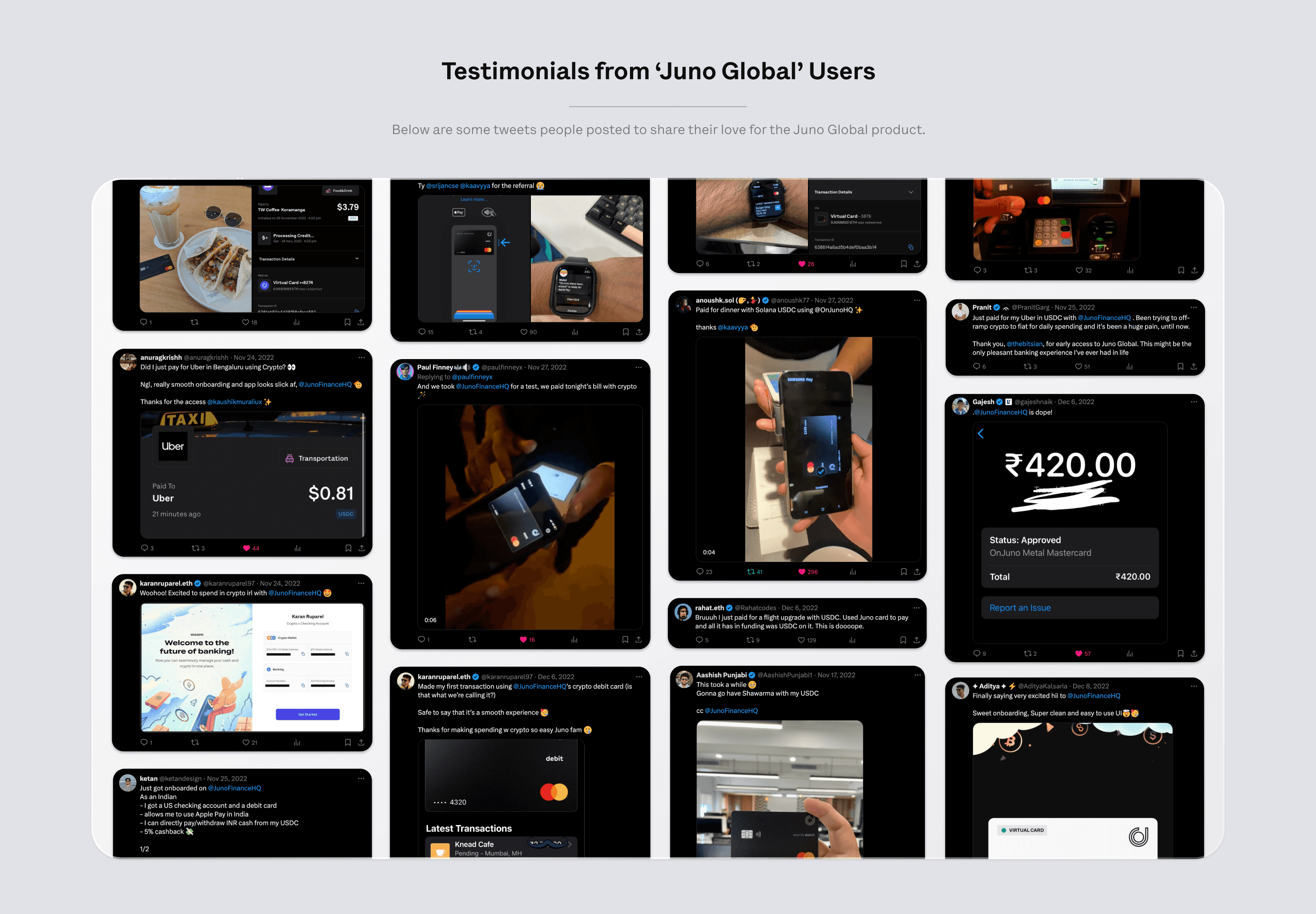

Nevertheless, we received a remarkable response from the community, with word-of-mouth spreading rapidly. The product became a topic of extensive discussion at ETH India 2022. Users were excitedly showcasing their experiences of spending crypto with Apple Pay and Google Pay on social media platforms like Twitter. While we had developed an innovative solution, unfortunately, the timing for its launch was not optimal.

Our focus had primarily been on the United States market. However, in September 2022, we expanded Juno's product globally and initiated a beta launch involving approximately 150 users from India and Dubai.

Despite having the technology and designs ready for the full launch, we encountered compliance hurdles with our partner bank, restricting further user acquisition and resulting in a halt to the product expansion.

The product remained available to users for 3-5 months. However, a limited beta user cohort only resulted in minimal movement in our business metrics.

Nevertheless, we received a remarkable response from the community, with word-of-mouth spreading rapidly. The product became a topic of extensive discussion at ETH India 2022. Users were excitedly showcasing their experiences of spending crypto with Apple Pay and Google Pay on social media platforms like Twitter. While we had developed an innovative solution, unfortunately, the timing for its launch was not optimal.

Our focus had primarily been on the United States market. However, in September 2022, we expanded Juno's product globally and initiated a beta launch involving approximately 150 users from India and Dubai.

Despite having the technology and designs ready for the full launch, we encountered compliance hurdles with our partner bank, restricting further user acquisition and resulting in a halt to the product expansion.

The product remained available to users for 3-5 months. However, a limited beta user cohort only resulted in minimal movement in our business metrics.

Nevertheless, we received a remarkable response from the community, with word-of-mouth spreading rapidly. The product became a topic of extensive discussion at ETH India 2022. Users were excitedly showcasing their experiences of spending crypto with Apple Pay and Google Pay on social media platforms like Twitter. While we had developed an innovative solution, unfortunately, the timing for its launch was not optimal.

Our focus had primarily been on the United States market. However, in September 2022, we expanded Juno's product globally and initiated a beta launch involving approximately 150 users from India and Dubai.

Despite having the technology and designs ready for the full launch, we encountered compliance hurdles with our partner bank, restricting further user acquisition and resulting in a halt to the product expansion.

The product remained available to users for 3-5 months. However, a limited beta user cohort only resulted in minimal movement in our business metrics.

Nevertheless, we received a remarkable response from the community, with word-of-mouth spreading rapidly. The product became a topic of extensive discussion at ETH India 2022. Users were excitedly showcasing their experiences of spending crypto with Apple Pay and Google Pay on social media platforms like Twitter. While we had developed an innovative solution, unfortunately, the timing for its launch was not optimal.

Learnings

I discovered that users were engaged in a 'Crypto Lifestyle - Earning and Living' cycle from 2020 to 2024. Apps are needed to empower users to earn in crypto and seamlessly spend it within the conventional fiat payment infrastructure.

I gained insights into the principles of exclusivity when developing our referral flows and understanding how to embed virality within the product to increase word of mouth. It's crucial to trigger users 'Aha' moment right at the onboarding stage.

I learned that for any financial app, prioritizing compliance is paramount. Even if it leads to launch delays, always putting customers and the security of their funds first is essential.

Users consistently value a positive user experience; providing innovative solutions to their challenges builds their loyalty over time.

I discovered that users were engaged in a 'Crypto Lifestyle - Earning and Living' cycle from 2020 to 2024. Apps are needed to empower users to earn in crypto and seamlessly spend it within the conventional fiat payment infrastructure.

I gained insights into the principles of exclusivity when developing our referral flows and understanding how to embed virality within the product to increase word of mouth. It's crucial to trigger users 'Aha' moment right at the onboarding stage.

I learned that for any financial app, prioritizing compliance is paramount. Even if it leads to launch delays, always putting customers and the security of their funds first is essential.

Users consistently value a positive user experience; providing innovative solutions to their challenges builds their loyalty over time.

I discovered that users were engaged in a 'Crypto Lifestyle - Earning and Living' cycle from 2020 to 2024. Apps are needed to empower users to earn in crypto and seamlessly spend it within the conventional fiat payment infrastructure.

I gained insights into the principles of exclusivity when developing our referral flows and understanding how to embed virality within the product to increase word of mouth. It's crucial to trigger users 'Aha' moment right at the onboarding stage.

I learned that for any financial app, prioritizing compliance is paramount. Even if it leads to launch delays, always putting customers and the security of their funds first is essential.

Users consistently value a positive user experience; providing innovative solutions to their challenges builds their loyalty over time.

I discovered that users were engaged in a 'Crypto Lifestyle - Earning and Living' cycle from 2020 to 2024. Apps are needed to empower users to earn in crypto and seamlessly spend it within the conventional fiat payment infrastructure.

I gained insights into the principles of exclusivity when developing our referral flows and understanding how to embed virality within the product to increase word of mouth. It's crucial to trigger users 'Aha' moment right at the onboarding stage.

I learned that for any financial app, prioritizing compliance is paramount. Even if it leads to launch delays, always putting customers and the security of their funds first is essential.

Users consistently value a positive user experience; providing innovative solutions to their challenges builds their loyalty over time.